Should you make a horror film?

The month of October seems a good time to look at films in the horror genre and we will be releasing a series of posts all month long that addresses the business of releasing these films.

Long the domain of ultra low budget filmmakers everywhere, horror audiences are now spoiled for choice when it comes to finding a film that terrifies. Yes, everyone with access to a digital camera and buckets of fake blood seems to be honing their craft and turning out product by the thousands. Unfortunately, most of it is high on splatter and low on story and production value. That may have made up the majority of the horror film sales 7 years ago, but distribution advances paid for such films are now exceedingly low (maybe $5K per territory, IF there is a pick up at all) and now the genre is perfect for the torrent sites.Unless you plan to make films as an expensive hobby, the pressure to produce a stellar horror film that people will talk about (see The Conjuring, Insidious, Paranormal Activity) is very high.

The trouble for filmmakers creating in this genre is there is so much being made of questionable quality, it is like asking audiences to find a needle…in a stack of needles (hat tip to Drew Daywalt). The same challenges for fundraising, marketing, and distribution that plague every production, plague horror films as well. To get good word of mouth, the film HAS to be great and have a significant marketing push.

At a recent event hosted at the LA Film School by Screen Craft entitled Horror Filmmaking: The Guts of the Craft, several involved in the horror genre talked about budgeting and distributing indie horror films. All agreed the production value bar has to be raised so much higher than everything else in the market in order to get people to part with their money for a ticket when competing with studio films. Talent manager Andrew Wilson of Zero Gravity Management pointed out that comments like the film did a lot with so little doesn’t hold water with audiences outside of the festival circuit. “You still need it to be good enough to get someone to come into a theater and pay $12…the guy who is going to pay $12 doesn’t care that you did a lot for a little bit of money. They want to see a film that is as good as the big Warner Bros release because they are paying the same amount of money to see it.” While you may be thinking, “I don’t need my film to play in a theater,” and that may be, the films seeing the most revenue in this genre are the ones that do.

The panel also addressed selling horror films into foreign territories. While horror does travel much better than American drama or comedy, there are horror films being made all over the world and some are much more innovative than their American counterparts. France, Japan and Korea were cited as countries producing fantastically creative horror films. American filmmakers with aspirations of distributing their films overseas need to be aware of the competition not just with fellow countrymen, but with foreign talent as well.

Other film distributors are candidly talking about the complete decimation of the market for horror, largely brought on by the internet and piracy, but also a change in consumer habits. Why buy a copy to own of that low grade splatterfest when you can easily stream it (for pay or not) and move on to the next one? More where that came from. There was once big money in fooling audiences to buy a $20 DVD with a good slasher poster and trailer, but now they are wise to the junk vying for their attention and don’t see the need to pay much money for it.

In a talk given last year at the Spooky Empire’s Ultimate Horror Weekend in Orlando, sales agent/distributor Stephen Biro of Unearthed Films actually warned the audience of filmmakers not to get into horror if money was what they were seeking.”The whole system is rigged for the distributors and retailers. You will have to make the movie of a lifetime, something that will stand the test of time.” He confirmed DVD for horror is dead. Titles that might have shipped 10, 000 copies to retailers are now only shipping maybe 2,000. Some stores will only take 40 copies, see how they sell and order more if needed in order to cut down on dealing with returns. Of the big box stores left standing, few are interested in low budget horror titles. Netflix too is stepping away from low budget indie horror on the DVD side. They may offer distributors a 2 year streaming deal for six titles at $24,000 total, but there will be a cost to get them QC’d properly (which comes out of your cut, after the middlemen take their share of course!).

As for iTunes, there are standards barring graphic sex for films in the US and in some countries, they are now requiring a rating from the local ratings authority in order to sell from the iTunes Movie store. The cost of this can run into the thousands (based on run time) per country. Also, subtitling will be required for English language films, another cost.

The major companies in cable VOD (Comcast, Time Warner, Verizon etc) are now requiring a significant theatrical release (about 15 cities) before showing interest in working with a title. They are predominantly interested in titles with significant marketing effort behind them. The cable operators often do not offer advances and you must go through an aggregator like Gravitas Ventures to access. If the aggregator refuses your film, that’s it.

Selling from your own site via DVD or digital through Vimeo or Distrify is still an option, and the cut of revenue is certainly larger. But unless there is a budget and plan in place to market the site, traffic won’t just materialize. Still, for ultra, ultra low budget films (like made for less than $5,000) with a clear marketing strategy and small advertising budget, selling direct is the way to go. Certainly better than giving all rights away for free, for 7 years and seeing nothing. At least your film can access a global audience.

Here is Biro’s talk from Orlando. It runs almost an hour

If after reading this, you are still set to wade into the market with your horror film, stay tuned to future posts looking at the numbers behind some recent horror films and what options you’ll have on the festival circuit.

photo credit: <a href=”http://www.flickr.com/photos/markybon/102406173/”>MarkyBon</a> via <a href=”http://photopin.com”>photopin</a> <a href=”http://creativecommons.org/licenses/by-nc-sa/2.0/”>cc</a>

Sheri Candler October 3rd, 2013

Posted In: Cable, Digital Distribution, Distribution, International Sales, iTunes, Long Tail & Glut of Content, Marketing, Netflix, Theatrical

Tags: Andrew Wilson, cable VOD, Distrify, Guts of the Craft, horror films, independent film distribution, iTunes, LA Film School, Netflix, Screen Craft, Spooky Empire's Ultimate Horror Weekend, Stephen Biro, Unearthed Films, Vimeo, Warner Bros, Zero Gravity Management

The Audacity of Hope: A Window into the Minds of Filmmakers at Independent Film Week

Next week (September 15 – 19) marks IFP’s annual “Independent FIlm Week” in NYC, herein dozens of fresh-faced and “emerging” filmmakers will once again pitch their shiny new projects in various states of development to jaded Industry executives who believe they’ve seen and heard it all.

Most of you reading this already know that pitching a film in development can be difficult, frustrating work…often because the passion and clarity of your filmmaking vision is often countered by the cloudy cynicism of those who are first hearing about your project. After all, we all know that for every IFP Week success story (and there are many including Benh Zeitlin’s Beasts of the Southern Wild, Courtney Hunt’s Frozen River, Dee Rees’ Pariah, Lauren Greenfield’s The Queen of Versailles, Stacie Passon’s Concussion etc…), there are many, many more films in development that either never get made or never find their way into significant distribution or, god forbid, profit mode.

So what keeps filmmaker’s coming back year after year to events like this? Well, the simple answer is “hope” of course….hope, belief, a passion for storytelling, the conviction that a good story can change the world, and the pure excitement of the possibilities of the unknown.

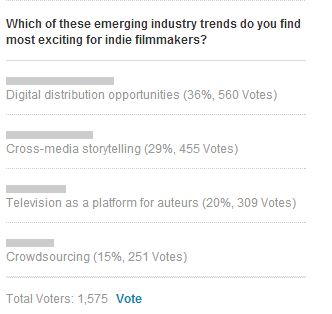

Which is why I found a recent poll hosted on IFP’s Independent Film Week website [right sidebar of the page] so interesting and so telling….in part because the result of the poll runs so counter to my own feelings on the state of independent film distribution.

On its site, IFP asks the following question:

Before you view results so far, answer the question….Which excites YOU the most? Now go vote and see what everyone else said.

** SPOILER ALERT — Do Not Read Forward Until You’ve Actually Voted**

What I find so curious about this is in my role as a independent film distribution educator at The Film Collaborative, I would have voted exactly the other way.

I suspect that a key factor in IFP Filmmakers voting differently than I has something to do with a factor I identified earlier, which I called “the pure excitement of the possibilities of the unknown.” I’m guessing most filmmakers called the thing most “exciting” that they knew the least about. After all 1) “Crowdsourcing” seems familiar to most right now, and therefore almost routine to today’s filmmakers….no matter how amazing the results often are. 2) “Television As a Platform for Auteurs” is also as familiar as clicking on the HBO GO App….even despite the fact that truly independent voices like Lena Dunham have used the platform to become household names. 3) Cross Media Story Telling remains a huge mystery for most filmmakers outside the genre sci-fi and horror realms….especially for independent narrative filmmakers making art house character-driven films. It should be noted that most documentary filmmakers understand it at least a little better. And 4) Digital Distribution Opportunities…of course this is the big one. The Wild West. The place where anything and everything seems possible…even if the evidence proclaiming its success for independents STILL isn’t in, even this many years after we’ve started talking about it.

But still we hope.

From our POV at The Film Collaborative, we see a lot of sales reports of exactly how well our truly independent films are performing on digital platforms….and for the most part I can tell you the results aren’t exactly exciting. Most upsetting is the feeling (and the data to back it) that major digital distribution platforms like Cable VOD, Netflix, iTunes etc are actually increasing the long-tail for STUDIO films, and leaving even less room than before for unknown independents. Yes, of course there are exceptions — for example our TFC member Jonathan Lisecki’s Gayby soared to the top of iTunes during Gay Pride week in June, hitting #1 on iTunes’ indie charts, #3 on their comedy charts, and #5 overall—above such movie-star-studded studio releases as Silver Linings Playbook and Django Unchained. But we all know the saying that the exception can prove the rule.

Yes, more independent film than ever is available on digital platforms, but the marketing conundrums posed by the glut of available content is often making it even harder than ever to get noticed and turn a profit. While Gayby benefited from some clever Pride Week-themed promotions that a major player like iTunes can engineer, this is not easily replicated by individual filmmakers.

For further discussion of the state of independent digital distribution, I queried my colleague Orly Ravid, TFC’s in house guru of the digital distro space. Here’s how she put it:

“I think the word ‘exciting’ is dangerous if filmmakers do not realize that platforms do not sell films, filmmakers / films do.

What *is* exciting is the *access*.

The flip side of that, however, is the decline in inflation of value that happened as a result of middle men competing for films and not knowing for sure how they would perform.

What I mean by that is, what once drove bigger / more deals in the past, is much less present today. I’m leaving theatrical out of this discussion because the point is to compare ‘home entertainment.’

In the past, a distributor would predict what the video stores would buy. Video stores bought, in advance often, based on what they thought would sell and rent well. Sure there were returns but, in general, there was a lot of business done that was based on expectation, not necessarily reality. Money flowed between middle men and distributors and stores etc… and down to the sellers of films. Now, the EXCITING trend is that anyone can distribute one’s film digitally and access a worldwide audience. There are flat fee and low commission services to access key mainstream platforms and also great developing DIY services.

The problem is, that since anyone can do this, so many do it. An abundance of choice and less marketing real estate to compel consumption. Additionally, there is so much less of money changing hands because of anticipation or expectation. Your film either performs on the platforms or on your site or Facebook page, or it does not. Apple does not pay up front. Netflix pays a fee sort of like TV stations do, but only based on solid information regarding demand. And Cable VOD is as marquee-driven and not thriving for the small film as ever.

The increasing need to actually prove your concept is going to put pressure on whomever is willing to take on the marketing. And if no one is, most films under the impact of no marketing will, most likely, make almost no impact. So it’s exciting but deceptive. The developments in digital distribution have given more power to filmmakers not to be at the mercy of gatekeepers. However, even if you can get into key digital stores, you will only reach as many people and make as much money as you have marketed for or authentically connected to.”

Now, don’t we all feel excited? Well maybe that’s not exactly the word….but I would still say “hopeful.”

To further lighten the mood, I’d like to add a word or two about my choice for the emerging trend I find most exciting — and that is crowdsourcing. This term is meant to encompass all activities that include the crowd–crowdfunding, soliciting help from the crowd in regard to time or talent in order to make work, or distributing with the crowd’s help. Primarily, I am going to discuss it in terms of raising money.

Call me old-fashioned, but I still remember the day (like a couple of years ago) when raising the money to make a film or distribute it was by far the hardest part of the equation. If filmmakers work within ultra-realistic budget parameters, crowd-sourcing can and usually does take a huge role in lessening the financial burdens these days. The fact is, with an excellently conceived, planned and executed crowdsourcing campaign, the money is now there for the taking…as long as the filmmaker’s vision is strong enough. No longer is the cloudy cynicism of Industry gatekeepers the key factor in raising money….or even the maximum limit on your credit cards.

I’m not implying that crowdsourcing makes it easy to raise the money….to do it right is a whole job unto itself, and much hard work is involved. But these factors are within a filmmaker’s own control, and by setting realistic goals and working hard towards them, the desired result is achieved with a startling success rate. And it makes the whole money-raising part seem a lot less like gambling than it used to….and you usually don’t have to pay that money back.

To me, that is nothing short of miraculous. And the fact that it is democratic / populist in philosophical nature, and tends to favor films with a strong social message truly thrills me. Less thrilling is the trend towards celebrities crowdsourcing for their pet projects (not going to name names here), but I don’t subscribe to a zero-sum market theory here which will leave the rest of us fighting over the crumbs….so if well-known filmmakers need to use their “brand” to create the films they are most passionate about…I won’t bash them for it.

In fact, there is something about this “brand-oriented” approach to crowdsourcing that may be the MOST instructive “emerging trend” that today’s IFP filmmakers should be paying attention to…as a way to possibly tie digital distribution possibilities directly to the the lessons of crowdsourcing. The problem with digital distribution is the “tree-falls-in-the-forest” phenomenon….i.e. you can put a film on a digital platform, but no-one will know it exists. But crowdsourcing uses the exact opposite principal….it creates FANS of your work who are so moved by your work that they want to give you MONEY.

So, what if you could bring your crowdsourcing community all the way through to digital distribution, where they can be the first audience for your film when it is released? This end-to-end digital solution is really bursting with opportunity…although I’ll admit right here that the work involved is daunting, especially for a filmmaker who just wants to make films.

As a result, a host of new services and platforms are emerging to explore this trend, for example Chill. The idea behind this platform (and others) is promising in that it encourages a “social window” to find and engage your audience before your traditional digital window. Chill can service just the social window, or you can choose also to have them service the traditional digital window. Crowdfunding integration is also built in, which offers you a way to service your obligations to your Kickstarter or Indiegogo backers. They also launched “Insider Access” recently, which helps bridge the window between the end of the Kickstarter campaign and the release.

Perhaps it is not surprising therefore, that in fact, the most intriguing of all would be a way to make all of the “emerging trends” work together to create a new integrated whole. I can’t picture what that looks like just yet…and I guess that is what makes it all part of the “excitement of the possibilities of the unknown.”

Jeffrey Winter will be attending IFP Week as a panelist and participant in the Meet the Decision Makers Artists Services sessions.

Jeffrey Winter September 12th, 2013

Posted In: crowdfunding, Digital Distribution, DIY, Film Festivals, iTunes, Long Tail & Glut of Content, Marketing

Tags: cable VOD, cross media storytelling, crowdfunding, Crowdsourcing, digital film distribution, Gayby, hope, IFP, Independent Film Week, iTunes, Jonathan Lisecki, Netflix, Orly Ravid, The Film Collaborative

Digital distribution AND marketing support is the aim of Devolver

Just prior to SXSW, I was contacted by a new digital distribution outfit called Devolver Digital Film who were launching during the festival. I rolled my eyes as I opened the email because frankly, digital distributors are becoming a dime a dozen and few offer anything that differentiates their services. Yes, they are all non exclusive, but most do not have much to offer in the way of audience recognition of the platform.

Film distribution in some fashion isn’t difficult to obtain anymore…but getting an audience to know a film is available, actively seek it out AND getting them to watch it is another story. So, I was intrigued to find out that Devolver is planning to help solve that problem. Devolver Digital Films is a company expansion out of video game publishing and distribution. Devolver is primarily known for the Serious Sam series of games and their success within the video game industry coupled with founder Mike Wilson’s filmmaking interests lead to a desire to use the same successful game marketing techniques for independent films.

The company’s first title, Cancerpants, is described as “a story about life, love, and a young woman’s journey with breast cancer.” Cancerpants is currently available on VOD networks Verizon and Frontier, and will reach Comcast, Cox, Cablevision, and Dish Online on June 4th. Local theatrical screenings are planned for May 30th in several cities including Grass Valley, CA (hosted by the filmmaker), Los Angeles, Austin, Houston, Oakland, and New York City.

I spoke with Andie Grace, VP of Acquisitions, and Mike Wilson, Partner and filmmaker, to hear what lead to Devolver’s foray into independent film distribution and what they plan to offer that other digital distributors don’t.

AG: “The experience that motivated the creation of Devolver Digital Films comes from the games space. Mike is also a filmmaker and he knows what it is like to run up against the wall of getting distribution. After spending years of making the film, getting your own network together, hitting the festival circuit and landing a distributor and then they put it out, but do little to support it. Devolver Digital would never put out a game that way and now there are so many films on the digital shelves too, a small film that is great could do a lot better with a little help.

When a filmmaker’s own network is exhausted, they themselves are exhausted and ready to move on to another project, they just need a partner to be interested enough to work the title and we saw it as a niche to be filled.”

SC: “Speaking of a niche, does Devolver have a niche audience that they are serving with films? My main problem with film distributors is they don’t really have an audience for their company. They are used to speaking to other businesses (exhibitors, video stores, broadcasters), but not speaking directly to any audience for their titles. Their titles are so diverse that they don’t even really know who is watching. Will this be a unique aspect for Devolver? Is there a Devolver audience?”

AG: “Genre fans definitely stick with a label because of what the label brings them. This is definitely true in the games space. We now have many gamers saying ‘What is my favorite game label going to do with movies?’ So our aim is to keep that fanbase alive and choose films we think they will like.

A lot of counter culture films are coming our way and I definitely look at those films and say ‘I know where to find people who will like this, I know how to organize events around this.”

MW: “Our brand will be built on films that we believe we can make bigger than they would have been without our help. Decisions on films will be based purely on what we think we can do with the network we already have in place. It won’t be according to genr. Inevitably everyone wants us to do films that are considered ‘gamer’ fare. But people who are outside of the gamer world don’t realize that gamers aren’t only into zombie movies or sci fi movies. The independent gamer tends to like lots of independent entertainment. Independent music, independent films, they tend to look a little further past the mainstream. More interesting, less predictable. So that is what we will specialize in.”

SC: “Is there something that the filmmaker has to bring with the project? Do they have to have a certain mentality? Do you want the filmmaker to be an active participant in marketing his/her work, or are you fine with them leaving it with you to make it successful?”

MW: “There are 2 kinds of filmmakers. Those that are exhausted from making the film and just want someone to take care of the rest for them. Some of those are very good films, but there is no promotional hook, and no niche we can tap easily. If they just want it out there, use our service to get it into the world, we’ll put it out for you and you can move on with your life.”

AG: “But we regard this as a partnership. We amplify what they have already started doing on their own. Anyone who wants to just turn tail and walk is probably not going to work well with us. Now, we do understand that by the time the film is ready for distribution, the filmmaker has already exhausted their network and they have done all they know how to do with their Facebook page or Twitter account and they need someone to help them, do it with them. It’s better for them to stay present, be there for the interviews, help craft the story, and use the opportunity to build their own brand as a filmmaker by working with us in a promotional partnership.”

SC: “What will be the range of services Devolver offers? I was thinking it was just digital distribution platforms, but you are working with Tugg to do events too?”

AG: “We will offer cable VOD and internet VOD right now. Being from the games world, we also have our eyes on gaming consoles. We will talk about the total distribution strategy based on the film. It may include using tools like Tugg to do some live event screenings rather than spending time exclusively on the festival circuit. Events can help power the VOD sales. We also will talk about the marketing and publicity, some of the more traditional tactics. We will motivate our own networks to help with promoting screenings. By having the film on VOD when it is in theaters, we can get it highlighted in the ‘in theaters now’ sections of Amazon Instant and such.”

MW: “We are going to be direct to the platforms when that is possible, but until we build up our catalog, it isn’t realistic to think we will be big enough to negotiate direct deals with the bigger players. With our zero overhead, we will be competitive with the percentages we take even when a third party is involved. Plus, we’re going to help promote it which should make the revenue bigger than it would if you went through an aggregator who isn’t doing that.”

![]()

SC: “Do you take rights over the film or do those stay with the artist?”

MW: “We wouldn’t take all rights like broadcast network rights, or international rights at the moment. But to the extent that we do put time in to exploit on certain platforms, we want exclusivity on those. It is just bad business for everyone if you have several companies pitching the same film. As a filmmaker, I know there are distributors who want to take all rights just in case in future they want to do something with them. That is not the case with us. Our reason for existence is to avoid that scenario, we have all experienced it as filmmakers ourselves.”

“We do ask for a minimum of one year with options to extend. Most cable operators do want a 5 year minimum. We have found on the games side that there are opportunities for digital bundles and we will want to include our films in bundles without having to keep going back to ask permission. We aren’t going to be releasing 30 movies a month or anything. The films we do have are precious to us and we will be working harder to make the small amount work for us and for the filmmaker.”

SC:”Advertising and promotion aren’t free, they often make up the majority of any kind of film release. Is this a service deal agreement where the filmmaker fronts the money for Devolver to spend or is this more like a traditional distribution situation where Devolver will front the money and recoup from revenue before the filmmaker sees any profit?”

MW: “This won’t be a six figure M&A budget. It is more like soft dollars from us in our organization and network of already existing connections. This is what helps support our games as well. Filmmakers will also be expected to help each other when they are on our label. So anything we provide from this network is just the cost of us doing business and we provide that.”

“Then, if there is an opportunity to buy into a promotional program or whatever, we’ll agree it with the filmmaker and write the check up front and share that cost. If the filmmaker gets a 60% split with us, we share the cost of the promotion.That’s the way we work in games too, it is purely situational. To the extent that they want to be involved, the filmmaker will sign off on any promotion we want to participate in and they will know the whole cost.”

“Another thing we feel is important is being completely transparent. If we do have to go through another distributor to get to a certain outlet, I will forward every royalty statement we get from that distributor so that the filmmaker knows what the revenues were. There has just been too much damage done by ‘Hollywood accounting,’ I use that term to mean all entertainment. The games industry is as bad as any. The little things we can do to remove any doubt about whether we are on the filmmakers team, we will do. The world may not need another VOD distributor, but one thing we will provide that others do not is transparency. There is always room for that.”

SC: “When is the best time for a filmmaker to approach you? In preproduction? Production? Post?”

MW: “I would say in post. We’re not a production company and we aren’t trying to influence the outcome of a movie. We can’t really have a conversation about a film until we know the level of quality it will be. Most of the people we are talking to are in fine cut or have a festival version that they still want to trim.”

AG: “We are having conversations now with people who are in post and it is pretty obvious who their audience is. We are also talking to people who are not going on the festival circuit, they are launching straight into distribution.”

MW: “We have many dream producers coming to us who get this online promotion stuff. We want to network them all together and help to promote each other.”

SC: “How will you bring them together?”

MW: “Google Hangouts I envision. I want just these producers who all have great ideas and are on the same label to get together and brainstorm with each other. Their films are all coming out near the same timeframe so I think some great creativity and excitement will come from it. I don’t think they imagine for a minute that helping someone else will hurt their own projects. It just makes their own network bigger, by aggregating everyone’s together.These are all young, smart, tech savvy producers who want to learn from each other.”

SC: “Well, that is definitely a differentiator for Devolver! Most distributors don’t bother themselves with bring together the filmmakers to help work with all the projects in the catalog. It means you really want to work with filmmakers who are giving, tech savvy and want to help make everyone’s work successful.”

MW: “The filmmaking process just sucks everything out of you, you are totally exhausted when finished and often you are the last man standing. The crew disappears after the wrap party. It will be great to have a company that knows this, pulls together a group of filmmakers in the same situation about to release their films and supports everyone.”

“It is really fun to be coming in at a time when we aren’t having to undo our skills. You go to industry panels where these veteran people are completely unsure of what is happening and frustrated at having to relearn everything because they are used to doing things in a certain way for many years. For us, it is exciting because it is wide open.”

I will be keeping an eye on this young and enthusiastic company. If you have a project you would like to approach Devolver Digital Films about, contact Andie Grace:

films [at] devolverdigital dot com

Sheri Candler May 9th, 2013

Posted In: Amazon VOD & CreateSpace, Digital Distribution, Distribution, iTunes, Netflix

Tags: Andie Grace, Cancerpants, Devolver Digital Films, Digital Distribution, digital distributor, independent film, Mike Wilson, Serious Sam, Tugg

Indie Game: a distribution case study

This article first appeared on the Sundance Artist Services blog on August 13, 2012

written by Bryan Glick with assistance from Sheri Candler and Orly Ravid

Indie Game: The Movie has quickly developed a name not just as a must-see documentary but also as a film pioneer in the world of distribution. Recently, I had a Skype chat with Co-directors James Swirsky and Lisanne Pajot . The documentary darlings talked about their indie film and its truly indie journey to audiences.

![]() Swirsky and Pajot did corporate commercial work together for five years and that eventually blossomed into doing their first feature. “We thought it would take one year, but it ended up taking two. I can’t imagine working another way, we have a wonderful overlapping and complimentary skill set, ” said Pajot. “We both edited this film, we both shot this film. It creates this really fluid organic way of working. It’s kind of the result of 5 or 6 years of working together. I don’t think you could get a two person team doing an independent film working like we did on day one. It’s stressful at times but the benefits are absolutely fantastic, ” said Swirsky.

Swirsky and Pajot did corporate commercial work together for five years and that eventually blossomed into doing their first feature. “We thought it would take one year, but it ended up taking two. I can’t imagine working another way, we have a wonderful overlapping and complimentary skill set, ” said Pajot. “We both edited this film, we both shot this film. It creates this really fluid organic way of working. It’s kind of the result of 5 or 6 years of working together. I don’t think you could get a two person team doing an independent film working like we did on day one. It’s stressful at times but the benefits are absolutely fantastic, ” said Swirsky.

According to Swirsky, Kickstarter covered 40% of the budget. “We used it to ‘kickstart’, we asked for $15000 on our first campaign which we knew would not make the film, but it really got things going. The rest of the budget was us, personal savings.” The team used Kickstarter twice; the first in 2010 asking for $15,000 and ended up with $23,341 with 297 backers. On the second campaign in 2011, they asked for $35,000 and raised $71,335 with 1,559 backers.

The hard work, dedication, and talent paid off. Indie Game: The Movie was selected to premiere in the World Documentary Competition section at the 2012 Sundance Film Festival winning Pajot and Swirsky the World Cinema Documentary Film Editing Award . “[Sundance] speaks to the independent spirit. It’s kind of the best fit, the dream fit for the film. Just being a filmmaker you want to premiere your film at Sundance. That’s where you hear about your heroes,” noted Swirsky. “Never before in our entire careers have we felt so incredibly supported…They know how to treat you right and not just logistics, it’s more ‘we want to help you with this project and help you next time.’ It was overwhelming because we’ve never had that. We’ve just never been exposed that,” interjected Pajot

They hired a sales agent upon their acceptance into Sundance and the film generated tons of buzz before it arrived at the festival resulting in a sales frenzy. The filmmakers wanted a simultaneous worldwide digital release, but theatrical distributors weren’t willing to give up digital rights so they opted for a self release. “There were a lot of offers, they approached us to purchase various rights. We felt we needed to get it out fairly quickly and in the digital way. A lot of the deals we turned down were in a little more of the traditional route. None of them ended up being a great fit,” said Pajot.

Several people were stunned when this indie doc about indie videogame developers opted to sell their film for remake rights to Scott Rudin and HBO. Pajot explained, “He saw the trailer and reached out a week or so before Sundance. That was sort of out of left field because it wasn’t something we were pursuing.” Swirsky added, “They optioned to potentially turn the concept into a TV show about game development…As a person who watches stuff on TV, I want this to exist. I want to see what these guys do with it.” The deal still left the door open for a more typical theatrical release. However that was only the start of their plan.

“We had spoken to Gary Hustwit (Helvetica). We sort of have an understanding of how he organized his own tours. We had to make our decision whether that was something we wanted to utilize. Five days after Sundance, we decided we would and were on the road 2 weeks after… Before Sundance this was how we envisioned rolling out…[We looked at] Kevin Smith and Louis C.K. and what they’re doing. We are not those guys and we don’t have that audience, but knowing core audience is out there, doing this made sense,” said Swirsky.

Lisanne Pajot and James Swirsky

They proceeded to go on a multi-city promotional tour starting with seven dates and so far they have had 15 special events screenings of which 13 were sold out! This is separate from 37 theaters across Canada doing a one night only event. They also settled on a small theatrical release in NYC and LA. When talking about the theaters and booking, they said theaters saw the sellout screenings and that prompted interest despite the fact that the film was in digital release. They accomplish all of this with a thrifty mindset. “P&A was not a budgetary item we put aside and if an investment was required, we would dip into pre orders. We didn’t put aside a marketing budget for it,” said Swirsky. Regarding the pre order revenue, they sold a cool $150,000 in DVD pre-orders in the lead up to release of the film. From this money, they funded their theatrical tour.

While the theatrical release was small, it generated solid enough numbers to get held over in multiple cities and provided for vital word of mouth that will ultimately make the film profitable. The grosses were only reported for their opening weekend, but they continued to pack the houses in later weeks.”I don’t look back at the box office. The tour was more profitable than the theatrical…They both have the benefits, having theatrical it gets a broader audience. It was more a commercial thing than box office,” said Swirsky. “We are still getting inquiries from theaters. They still want to book it despite the fact it’s out there digitally,” said Pajot. “We had this sort of hype machine happening. We didn’t put out advertising. Everything was through our mailing that started with the 300 on our first Kickstarter and through Twitter,” said Swirsky. Now the team has over 20,000 people on their mailing list and over 10,000 Twitter followers. In order to keep this word of mouth and enthusiasm going, the filmmakers released 88 minutes of exclusive content – most of which didn’t make the final cut – to their funders, took creative suggestions from their online forum and sent out updates on the games the subjects of their film were developing over the course of the two years the film was in production.

Following the success the film has enjoyed in various settings, Indie Game: The Movie premiered on three different digital distribution platforms. If you were to try and guess what they were though, you would most likely only get one right. While, it is available on the standard iTunes, the other two means of access are much more experimental and particularly appropriate for this doc.

It is only the second film to be distributed by VHX as a direct DRM-free download courtesy of their, ‘VHX For Artists‘ platform. Finally, this film is reaching gamers directly through Steam which is a video game distribution platform run by Valve. This sterling doc is also only the second film to be sold through the video game service, where it was able to be pre-ordered for $8.99 as opposed to the $9.99 it costs across all platforms. This is perhaps the perfect example of the changing landscape of independent film distribution. Every film has a potential niche and most of these can arguably be reached more effectively through means outside the standard distribution model. Why should a fan of couponing have to go through hundreds of films on Netflix before even finding out a documentary about couponing exists, when it could be promoted on a couponing website?

As they are going into uncharted territory, both Pajot and Swirsky avoided making any bold predictions.”It’s just wait and see. It’s an experiment because we’re the first movie on Steam. We’re really interested to look at and talk about in the future. I don’t want to make predictions…I do think documentary lends itself to that kind of marketing though. We’re trying to not just be niche but there is power in that core audience. They are very easy to find online,” said Swirsky.

Just because they are pursuing a bold strategy doesn’t mean they were any less cost conscious. “The VHX stuff, it was a collaboration, so there were no huge costs. Basically subtitles, a little publicity costs from Von Murphy PR and Strategy PR who helped us with theatrical. Those guys made sense to bring on,” said Pajot. “A lot of our costs were taken up by volunteers. If they help us do subtitles, they can have a ticket event, a screening in their country,” added Swirsky.

They also note that a large amount of their profit has been in pre-orders. 10,000 people have pre-ordered one of their three DVD options priced at $9.99, $24.99 and a special edition DVD for $69.99 tied with digital. While the film focused on a select few indie game developers, they interviewed 20 different developers and the additional footage is part of the Special Edition DVD/Blu-Ray. That might explain why it’s their highest seller.

All this doesn’t mean that any of the dozens of other options are no longer usable. Quite the contrary, they have also taken advantage of the Sundance Artist Services affiliations to go on a number of more traditional digital sites. Increased views of a film even if on non traditional platforms can mean increased web searches and awareness and could be used to drive up sales on mainstay platforms.

The real winner though is ultimately the audience. For the majority of the world that doesn’t go to Sundance or Cannes each year, this is how they can discover small films that were made with them in mind. The HBO deal aside, this is bound to be one incredibly profitable documentary that introduces a whole new crowd to quality art-house cinema. “We are still booking community screenings. If people want to book, they can contact us…We are thinking maybe we might do another shorter tour at some point,” said Pajot.

Here’s to the independent film spirit, alive and well.

Update Feb 2013: The creators of Indie Game have written their own case study discussing the many tools and techniques they used. Head over to their website for the full study.

Orly Ravid August 16th, 2012

Posted In: Digital Distribution, Distribution, DIY, Film Festivals, iTunes, Marketing, Publicity, Theatrical

Tags: crowdfunding, DIY distribution, documentary, game developers, Gary Hustwit, independent film, Indie Game, James Swirsky, Kevin Smith, Kickstarter, Lisanne Pajot, Louis C.K., self distribution, Steam, Sundance Artists Services, Sundance Film Festival, VHX, VHX for Artists

European distribution series: OnlineFilm

By Sheri Candler

Here is the second part in a series on European distribution tools. I met OnlineFilm AG CEO Cay Wesnigk, based in Germany, while attending the FERA General Assembly in Copenhagen. Like most people in attendance, he is trying to understand the repercussions and opportunities of the online space to the film industry. His response was to come up with a solution that allows filmmakers themselves to profit and to spread their work to territories outside of their home country by using the internet.

SC: What does OnlineFilm hope to accomplish for European filmmakers and film audiences?

CW: The Onlinefilm.org System is a multilingual marketplace for films and an application service provider for digital distribution and marketing services, owned by a collective of independent producers/ filmmakers. Any rights owner from all over the world can use its technology to offer films as download to own and stream to rent or both.

To reach these goals, we want to strengthen and enlarge our network of national partners that are running the Onlinefilm.org system in their territories and run national websites that use the same technology to develop local markets. Together with our partners we want to develop new tailored ways of marketing by using social media and viral campaigning in their languages and territories and then learn from each other and teach our best practice examples to the film makers to empower them to use the onlinefilm.org system in the best possible way to market their films.

Our motto is “Films are made to be seen” and we want to make it possible for the international audience to access the films they are interested in and find those they did not know existed, helping the makers to find and access their audience.

SC: Do you think the audience is ready to start watching full length films online or on mobile devices?

It should be added to the question, “legally aquired” films. I think it is a proven fact that our audience is watching films on those devices, just go through a train in Europe and you will notice how many people are watching films on laptops and tablets, some even on smart phones. In catalogues of supermarkets, hard disks are offered that have a connection to regular TV and a remote control as well as Network access that make it easy to bring downloaded films to the TV screens. For us, the question is not if there is an audience out there for our films, the question is, is there an audience willing to pay for them?

But there is another angle to your question, a topic for online watching of films is the deceleration of the audience. It is difficult to watch 90 minutes linear programming with no interaction expected on a computer or tablet when the IM Messenger pops up, the Skype rings and your email program reminds you that a new mail has arrived in your mailbox… For that we need to find ways to decelerate our audience. One is the easy connection of the device with the TV set as mentioned above. Leaning back in front of the TV with the mouse out of reach is half of the trick. The other half still has to be developed.

SC: There are already many online streaming platforms for films, many of them are free streaming and ad supported streaming. What is the plan for driving audience interest to OnlineFilm?

CW: A film is a little bit of celluloid and a lot of marketing…

We have experienced that many film-makers do not promote their films once they have upload them in to the system by using the tools and strategies actively that we supplied for them. Some of them do not even link to the films from their own homepages, let alone think about how to promote their films through other channels that would generate audiences for them. Even a good Google ranking for film titles searches that we can supply does not bring the revenue, since for that, the customer has to know that a film exists and must actively search for it. So we have drawn the conclusion that we must act more on the filmmakers behalf to create more sales and such make the option to offer films through the Onlinefilm.org system more attractive. One measure we took was the cooperation with other outlets and websites by offering them tailored Mediatheks for their visitors, creating more outlets and chances that audiences will find a film by chance.

The next step will be to create best practice examples through social media campaigns that will lead to more sales of the promoted example films.

We offer tools to the filmmakers to help them create their own audiences. We offer at the same time a Platform for curators, for the hunters and collectors. They can use the search tools the site offers them to find the raw diamonds. They can browse through the categories, use our full text search in German and English or search for directors or film titles they might already be aware of.

Film of the week on the OnlineFilm homepage

The film of the week section on the landing page of www.onlinefilm.org can change its focus on three different film categorie; Docs, Short- or Feature films, or offer a mixture of all of them (default). With this preselection we want to promote films to people who just drop by our platform with no special film or interest in mind. We often change the selection and try to keep the offer interesting and diverse so every visitor should find something of interest to him and, if not, might be motivated to dig deeper into the catalogue, to find out more about its wealth of topics and genres.

In the second line “the featured films”, the recommendations also changes accordingly once a customer selects where his point of interest lies (docs, short, feature). If someone tells us he is interested in shorts, the site will offer him different shorts. If he tells us he likes docs, he will be offered mainly docs. This is how we try to keep our first time visitors on the site and offer them selected films out of our large catalogue that might be of interest for them. The more we get to know from a visitor on the site, the more we want to tailor the offers made to his interests.

Our national portal Strategy – many different editorial lines

If a visitor decides to “explore the Network” he will be guided to the overview map with all national sites that are active so far. He can then select one of them, where our national Partners have the editorial control, offer national content or content they consider interesting for their fellow country man. Their editorial line is subjective. They will offer the films from their country and others they have found in the system and deem interesting for their audience. We plan to extend the editorial possibilities of the partner pages so the partners will also have their own film of the week and other editorial possibilities to promote certain films on their sites.

By creating sub portals with a special focus, it is also always possible to follow a new editorial line if enough films to justify that are in the system..

Our Greek partners www.greece.onlinefilm.org are the most advanced, they have been with us right from the very beginning of the project in 2007 and they also have made the most out of the technology that onlinefilm.org has offered them so far. As an example, on their editors page, they made their own sub categorisation and such made it possible to browse through the films via topics they have selected on their own.

Greek director Roviros Manthoulis’ collection page

They also have published the Roviros Manthoulis collection and make it possible to browse through the films of this renowned Greek filmmaker. Both serve as an example for an individual editorial line of a partner portal.

Another example is Ireland.onlinefilm.org. Our Irish partner has chosen quite a ew titles from the system and publishes them on his site. Among them a French/Greek film called IRLANDE: LA MEMOIRE D’ UN PEUPLE about Ireland and its music in the 70s. This film has become quite popular on the Irish website and no one in Ireland would ever have known about this document of Irish folk music if it would not have been uploaded by our Greek partner and found and published by our Irish partner. Also interesting to note is that our Irish partner translated the site into Gaelic language, another way to make the site something special. We use a multi language editor that makes it possible to translate any of our sites in as many languages as necessary.

Since it is always also possible for any rights owner to upload any film from anywhere, we have many films from countries where we do not have a partner installed yet. The more films we get from one country the more active our search for a partner there becomes. We always offer anyone who uploads at least 30 films to get his own Macro shop. This would entitle him also to get a promoter percentage of 8% for any customer that enters the System through his shop. If the relationship develops well and we see the person is active and well connected, he can apply to become a national partner and will then be able to also add other films he has not uploaded into his shop. If he is willing to invest into the cooperation, he can apply for full partner status that would also guarantee him part of the revenues any film uploaded from his territory might generate as a partner percentage. An example of a tailored Macro shop of a German distributor is here: www.filmgalerie451.onlinefilm.org

This is how we slowly built our Network of national partners and built more and more local outlets with their own editorial line.

Some more examples you will find here

www.kurzfilmtage.de/videothek the Videothek of the Oberhausen Shortfilmfestibval, run with onlinefilm technology and with Onlinefilm films

www.freitag.onlinefilm.org A videothel of a German Newspapers Website, run on onlinefilm technolog and with Onlinefilm films

SC: Is this platform mainly for German films or is the focus on all foreign language films?

CW: Any one can upload a film no matter where he or she comes from. We encourage people to upload the film in its original language version and in English. Subtitles are sufficient. More language versions can be uploaded and offered for different self chosen conditions. We even offer a tool ( in Beta) with which one can create subtitles to a film which is uploaded into our system and save and offer them. Subtitles can also be imported into the tool and exported into many formats if produced with the tool. The subtitle tool is designed in a way that a filmmaker could ask a professional or friend in another country to create the subtitles of a film he has uploaded. We are also planning to create a system to allow a person who has created subtitles to opt in and get a piece of the revenue as remuneration for his work, any time the film is watched with his subtitles.

SC: What prices are being asked of the audience to pay?

CW: The price per download or stream is defined by the rights owner who offers the film via the onlinefilm.org system. Over the last 2 year,s the average download price per title has increased from € 2,50 (2008) to € 5,00 in 2010 and to € 6,00 in June 2011 (from a range between € 0.99 and € 16,00). Our bestseller right now costs € 8,50 per download (around $10 USD).

SC: How do you handle payments on the system for all different currencies? Can those not on the Euro still use the OnlineFilm system? How about those who don’t have credit cards?

CW: Right now you pay via Paypal in Euro, that works also with a credi card via Paypal guest status, then you can stream or download the film direct when redirected by Paypal after the payment is done on their server. We are looking into possibilities to offer films in different currencies viaPpaypal right now and hope to offer that kind of service in the near future!

As an alternative, we already offer payment through international bank transfer via IBAN and BIC to our account in Germany. Once the money is sent to our onlinefilm account, the buyer sends us a pdf with the view of the online money order ( screen shot or what the online banking software offers) and we sent him or her the download links via e mail or put the film for streaming into his or her account at onlinfilms under “my films” This sometimes takes a few hours to fulfill but it is better than nothing. So far it has been used mainly by Paypal haters.

SC: What is the revenue split for filmmakers? Are there any fees that have to be paid for the films to use OnlineFilm?

CW: No fees are asked just to offer the film on onlinefilm.org. If you just use the system to host trailers/teasers and use our promotion tool to send free downloads and streams to selected people, but you do not offer the film for payment to a general audience, we would ask you to pay for used bandwith and storage. But there is a free amount of traffic per month, sufficient for trailer hosting of average films, that anyone can use before that happens.

The revenue is split as follows. 51% of the turnover always goes to the producer/ rightsowner. If the rightsowner buys 1.000 shares of the Onlinefilm AG and such becomes co-owner of the system ( option) he can get 5% more which then ads up to 56% . If he sells the film via an embedded shop or Macro shop from his own page and opts in for the affiliate percentage, he will get an extra 8% which then makes his or her revenue climb up to 64% of the sales price (the Affiiliate system still has to be implemented).

SC: What kinds of films are doing well at the moment? documentary, horror, drama? What might these successes all have in common? Do they have notable names, festival accolades, strong coproduction deals that have given lots of promotion, great mainstream media reviews?

CW: We mainly have quite old films on the platform so far, this has many reasons in copyright issues unclear, release windows and power play of the old gatekeepers trying to hinder the films going online all together. Only very few of the films could profit directly from any marketing campaigns.

The films that are successful right now have a campaign behind them or at least some promotion mostly done by the filmmaker via personal website or mailing list. The others are just occasional sales by active seekers for exactly that title. They live on their past time fame.

One very successful 15 year old film Deckname Dennis is a first part of a film called Die Mondverschwörung presenting the same character and using the same technique, that has been released theatrically recently. Through the press the new film received and by creating a social media campaign for the new film that clearly stated its predecessor was available online (Facebook, Youtube, a website, Twitter) we made that film popular again. You might say it went viral and made quite an impressive turnover for its rightsowner. To download the film, the price is 8,50 Euro. We were extremely happy that through a good text the director posted in the blog of a pirate site where the film was also available, we got them to link to our legal offer and take down the illegal offer. Through our link statistics, we can see that many people come from there to us.

SC: I know that the German film industry is particularly concerned about online piracy, how does a site like OnlineFilm help alleviate this concern?

CW: We do not use DRM systems simply because we do not believe in them and we do not want to make it difficult for the customers. Also we do not want to greet our customers as criminals that we do not trust. We follow the principle of “digital rights fair trade” in short “do not bullshit your audience and your audience won’t bullshit you”. Our download is DRM free, whoever buys it will also be able to download the film again, when he needs to. He just needs to log in with his username and it will be in the “my films” section. Since our streaming technology is “dedicated flash streaming” it is not quite as easy to save the stream as with other techniques. The stream is rented for 48 hours and usually cheaper than the download, but it can also be offered solely if people want to better protect their work and do not want it downloaded.

SC: Is there a geoblocking mechanism on OnlineFilm so that if a filmmaker has sold a online sales territory or has a sales agent looking to sell a territory, that territory is blocked? I know that many sales agents ask for a hold back timeframe on titles so they can sell those territories around the world. Is the site mainly to exploit titles that are no longer active in the marketplace? In effect, taking films out of the “library” mode and putting them back out into the marketplace?

CW: At the moment we do not offer geoblocking. Anyone half clever seems to be able to enter any system with a false IP and ridicule these mechanisms. Secondly, we think if a customer wants to legally purchase a film we should sell it to him and not tell him to go elsewhere (namely the pirate sites). We will nevertheless implement an IP scan and geolocation tools in the near future. We have to since the industry seems not to change its ways as fast as it should. We hope to be able to serve the customer by offering a revenue share with the person or distributor who has the rights in the territory where the customer comes from. But this might still take while to program and implement.

SC: Does OnlineFilm do any marketing on the part of the titles? Or is the filmmaker expected to conduct their own marketing strategy to drive traffic to the site?

CW: Onlinefilm does marketing for the site and through the many partner sites also tries to drive more traffic towards the films. We also market some titles that we select via our onlinefilm Facebook page and via the film of the week and the recommendations on the landing page. We have a space on the Kulturserver Network where we can promote individual titles.

When our staff has time left, we also try to encourage links to topic driven films from topic driven websites. We offer marketing support for filmmakers that are open for it, but we ask for a fee if they want a campaign run by us. Then we try to build a social web campaign with them and show them how to, or do the job for them depending on their skills and time or money they want to invest.

This is something we definitely need to put more energy in because far too many filmmakers here do not know how to self promote their films and rather invest their time in making a new one. The revenue made online with many of the films is so far not big enough to encourage distributors or filmmakers to invest a lot of time or money in extra marketing. But since we see that the turnover with films is growing constantly, we hope that this will change and lead to an exponential growth of sales once people will be willing to invest more in marketing once they see the potential.

We are preparing a social media campaigning and online marketing handbook. At the same time we are trying to connect with people who specialize in the craft of online film marketing. We want to develop business models with them that will work for them and the rights owners possibly also on a revenue share basis.

My thanks to Cay Wesnigk for taking the time to talk with us and explain how his company is helping European filmmakers make the shift from a primarily cinema driven distribution model to an online one.

Orly Ravid July 25th, 2012

Posted In: Digital Distribution, Distribution, Distribution Platforms, Facebook, Marketing

Tags: Cay Wesnigk, Copenhagen, download, DRM, European Digital Distribution, featured films, FERA, geoblocking, Germany, Greece, Ireland, online film distribution, OnlineFilm, Paypal, Roviros Manthoulis, streaming

Lead up to Cannes: Digital Distribution Beyond the Old World

This post was originally published on the Sundance Artists Services blog on April 23, 2012. This is an interview between Rights Stuff’s Wendy Bernfeld and The Film Collaborative’s Orly Ravid on the state of digital in Europe

In the past, many new media and VOD platforms – whether based on pay-per-transaction (TVOD), subscription (SVOD), free to user/ad supported (ADVOD) or download to own (DTO) — came and went, to the disillusionment of those brave souls trying to explore and develop the new sector and audiences.

Some filmmakers, sales agents, distributors who dared to license were wonderfully pleased with surprisingly good results for particular films (and not always the same ones that were mainstream successes in traditional media), but on balance, let’s face it, most were underwhelmed with the lackluster performance or transience of the various sites, and eventually became jaded about the whole sector. But it’s no longer a viable option just to sit back.

Over the past 18 months particularly the digital/VOD sector (including internationally) has finally begun paying off well for filmmakers, producers, distributors, and sales agents… at least for those who are willing to take the time to navigate (alone or partnered with others) the complexities of the sector, play with creative ”windowing’’ while balancing opportunities from traditional media, and accept initially more modest revenues from multiple smaller deals across various platforms and regions (yielding cumulative revenues in a largely non exclusive sector).

In addition to traditional media deals and VOD deal potential with IPTV, telecom, and cable offerings, and larger American sites (e.g. Hulu, YouTube, Netflix, iTunes), your film may well find interested audiences and homes on EU/international platforms…even if not picked up in the USA.

HOW IS INTERNATIONAL DIGITAL DIFFERENT FROM THAT IN THE USA?

The EU (beyond UK) deals with multiple languages, different tastes and appetites, different windows (vs consistent release patterns/dates per country), different platforms to navigate and balance against multiple different traditional media buyers, and, to be honest in general more work for smaller potential revenues from each deal/window.

But on the plus side, films can find homes overseas in many markets and windows, even if not ending up in the mainstream or major US/UK platforms.

The UK is at the moment probably the more stable and lucrative for English (the VOD market is already very competitive, with large platforms like Netflix, Lovefilm, BSkyB, FilmFlex, iTunes, and Blinkbox) but as soon as you ripple out to EU, digital distribution will take more work and art and generate relatively less money, especially if your film is only in original English language, and not already exposed in terms of promo/PR (theatrical, DVD release in the region etc.). However, there is indeed a growing appetite by now for art house, festival, docs, quality indie films, and foreign language films, if well curated, e.g. around festivals/brands/themes rather than as one-offs.

WHO’S OUT THERE in EU and what are some of the key territories where digital is meaningful?

Digital is immediately more meaningful in the UK, France, the Nordic region, and in Benelux, where there are already pc/mobile and tech-savvy customers and a willingness to view films in English with subtitles (vs. the dubbed regions of Germany, Spain, Italy etc., where one has to invest more to get the languages to cross over).

Although publications often refer to figures noting several hundreds of VOD platforms in Europe, in my view there are only probably 100 or so that are worth talking about when discussing licensing—half of which the main revenue generators, and another half of which are still potentially significant buyers(depending on the film of course)

In Europe, as in America, transactional VOD (pay per view) platforms are more established – some regional (per country), and others multi region (e.g. Acetrax, UPC/Chello, Headweb, iTunes, Playstation Network Live, Voddler, Xbox Live). Outside of the UK, one obviously enhances possibilities if addressing customers in their own languages and tailoring content to local preferences such film classification, advertising, and general consumer and cultural tastes.

iTunes has only recently (in autumn 2011) begun to expand its footprint into Europe, including in the following EU countries: Austria, Bulgaria, Cyprus, Czech Republic, Denmark, Estonia, Finland, Greece, Hungary, Latvia, Lithuania, Malta, Netherlands, Norway, Poland, Republic of Ireland, Romania, Slovakia, Slovenia, Spain, Sweden, and the United Kingdom. Non-English stores include: Spain, France, Germany, Italy, Luxembourg, Belgium, Switzerland, and Portugal. They also just recently launched in Brazil / Latin America as well.

NETFLIX, Amazon (via Lovefilm), and Hulu are expanding their international footprint too. Netflix, for example, recently launched in UK/Eire, and is anticipated to roll into other regions such as Spain thereafter, and has already extended its occasionally original production commissioning activities to EU (e.g. Denmark – Lillyhammer deal, and more recently France (Gaumont etc) – Hemlock Grove series funding ). Lovefilm already has a presence beyond the UK (in Germany and Nordic), and is anticipated to expand regions. Hulu has not yet launched in EU but did launch already in Japan. As part of its competition rampup (in the US against Netflix in the SVOD market, it has also began commissioning original programming, (Day in the Life – Morgan Spurlock, for example, which was just picked up by Fremantle for distribution thereafter)….and also continues seeking special films or shows to do stunts around. We understand that they are trying to acquire more Spanish rights for the US…an important strategic move for other US players trying to expand their footprint in EU as well. Meanwhile in early 2012 the UK became a hotbed of activity for SVOD, with deals that would formerly have been nonexclusive (with e.g. Netflix, Lovefilm) being now struck on a lucrative exclusive basis, following the example of the competitive SVOD vs. Pay TV market in the US.

So what are the other key EU platforms? Trends?

Various international platforms are now becoming increasingly interested in licensing more art house, niche and festival films–not just mainstream titles. It is expected that some of the larger brand sites this year (e.g. those in UK like Netflix, Lovefilm, etc.) will expand the indie/art house and festival category further, and also be open to foreign language films (dubbed or subtitled as applicable per country audience as above). Most deals for art house/fest films, where not locally versioned or released in theatres or DVD, are on a non exclusive rev share basis, and in some cases where there is particular acclaim or cast, it can be coupled with a modest upfront, while if on an SVOD basis, flat fee deals apply (similar to non-exclusive Pay TV licensing deal parameters).

But in countries where the Pay TV incumbent is competing against a new web player, such as a traditional Pay TV player “vs.” SVOD (like Netflix “vs.” HBO in the US, or Lovefilm/Amazon “vs.” BSkyB in UK), as above, the fees can be more lucrative, in the form of true flat license fees in the Pay TV range. – whether on exclusive or non exclusive basis, and thus matching or exceeding the normal price ranges before the competition. As well, when competition heats up over one category of title, it’s also not unusual to have the competitors round out, extend, or diversify their consumer offer and move into other genres, to try to distinguish themselves from the competition. This is happening in more and more countries– for example the Netherlands, where HBO /Ziggo just launched in February and the local incumbent, Film1, responded by adding a branded art house/indie thematic channel (Sundance Channel).

Key note: Deals are generally non-exclusive and thus if carefully staggered, one can license the film sequentially through various windows (TVOD, SVOD, AVOD, and if applicable, DTO) and in multiple regions.

An example: one can first license a current film for transactional VOD (TVOD) on a rev share basis to cable and telecom VOD platforms (like France Telecom/Orange, UPC, etc) as well as (simultaneously) web based players (e.g. iTunes), then to subscription -based windows (premium Pay TV (e.g. HBO, Viasat) and their corresponding “TV Everywhere” offerings, thematic Pay TV, and/or standalone SVOD services . Thereafter, the film can move to other ad-supported services (free to consumer, web based, e.g. YouTube AVOD). This pattern can apply in multiple countries.

As mentioned above, there are hundreds of local European platforms —both standalone web-based services and mainstream and/or local telecom and Cable VOD platforms that have online offerings of their own. VIASAT, for example, was historically a premium pay service, but now offers not only conventional Pay TV and ”TV Everywhere” but also standalone thematic offerings to non-subscribers (SVOD to PC). Similarly, BSkyB just announced the upcoming launch of NOW TV – also aimed at non- subscribers (“Cord Nevers, and/or Cord Cutters”) – a thematic SVOD/low pay offering of films.

Opportunities will only increase in 2012 and 2013 as more from USA players, sites, and OTT box offerings beyond Netflix, Hulu, and Amazon gradually cross over to EU/international markets particularly if the new services don’t limit themselves to mainstream offerings and tastes.

Getting to the platform: As in the United States, some of the larger platforms (such as LOVEFILM, BlinkBox, Netflix, itunes) only take larger packages of films with a minimum volume, and are unwilling to deal direct with producers and distributors for “one off” deals. Until recently, most of the larger sites also focused mainly on mainstream films. In general, these services steer filmmakers towards conventional distributors, or aggregators/digital distributors like Movie Partnership (UK); but sometimes will accept dealings direct for certain films, or will go via an agent working on a flat fee basis (like Rights Stuff / Film Collaborative). In the latter scenario, the film IP remains in the filmmaker’s/distributor’s name, the money from deals flows to them directly and they get access and paid advice through third party consultants/agents/advisors.

Up until now, having had a DVD and/or local theatrical release was quite important for enhancing deals. But increasingly now online sites are willing to handle more innovative windows, e.g. premiering films online, or Day & Date with other windows (or shortly thereafter). Lesser-known or library (catalog) films can usually find a home on a non- exclusive and on ad-supported (AVOD) basis, but more current films usually start with transactional (TVOD) basis and/or subscription platforms (SVOD)… If filmmakers have titles already encoded to the expensive iTunes spec, this can be helpful in wider distribution, but it’s not essential; many digital platforms are now willing to take delivery of indie or art house films even via DVD or a hard drive/ digital master.

In terms of deal models, some aggregators (middlemen) take larger %s but then take care of all encoding and delivery fulfillment, while others who are more in an advisory or agent role take a lower share for deal making and platform access but leave you to arrange the encoding separately. In some countries (e.g. Brazil), platforms may not take English versions unless local subtitles or dubs are available, and work with distributors who create versions where necessary. These distributors co-curate packages with filmmakers based on experience of what “moves” best in the region so as not to invest in encoding or language versioning for films that may not generate enough revenue to justify it…

A side note regarding subtitling, by the way: Film Collaborative is looking into software that helps facilitate dubbing in the same voice as the actor/speaker, but meanwhile in any case, subtitling for digital is getting less and less expensive and can be done via relatively inexpensive software or labs. If one has shown a film at a film festival in another country and plans to then distribute the film there, we’d recommend you ask the fest for access to the subtitles (if cleared for other distribution). Traditionally, Nordic, Benelux, and some other regions are fine with and prefer subtitles, while others (such as Germany, Spain, and Italy) require dubbing. However, in the higher-educated arthouse/filmfest world, one can often get away with just subtitled versions even in the dubbing countries.

As indicated above, for better platform access, one may want to pick or join with new media /digital distribution specialists – particularly if your traditional sales agent or distributor, strong in conventional media (theatrical, video etc.) is however not active or savvy in the VOD landscape above (platforms, deal terms, contacts etc). Otherwise it can be a self-fulfilling prophecy that you then ”don’t make money in digital’’. It’s a balancing act of cost vs. services, and a lot of work in international!

And filmmakers, whatever you choose to do with respect to your digital distribution, do not forget that one can also reach the whole wide world via one’s own website(s) and social networking pages by utilizing DIY digital distribution services (for more on this topic please refer to numerous past blog posts about digital distribution and DIY platforms and services at www.TheFilmCollaborative.org/blog and/or the Resource Place at www.TheFilmCollaborative.org/ResourcePlace).

As for piracy: in various cases filmmakers can tap into or derive indirect benefit from these online communities. See for e.g. Sheri Candler’s case studies in www.SellingYourFilm.com, Some filmmakers partner with Bit Torrent, Pirate Bay etc to launch their films online, tapping into the audiences already there (e.g. Nasty Old People, The Tunnel, Yes Men Fix the World).

LET’S TALK ABOUT POTENTIAL FUTURE TRENDS:

Diversification, Cross Platform/Transmedia: We believe 2012 will see continued consolidation of platforms and fuller diversification within the genres offered. Also as above, some key platforms (such as Hulu, Netflix, Yahoo, Endemol/AOL, Nokia, Canal+, Orange, ARTE, Channel4, ) are now also selectively commissioning transmedia and/or branded film opportunities (YouTube has not begun funding outside US yet). New funds and educational bodies (including MEDIA, Power to the Pixel) are increasing the emphasis on digital as a 360 proposition from inception of the film production process.

Multi-Layered Business Models: Platforms’ business models are also starting to become more multi-layered to handle different genres, consumer price points, and windows. For example, AVOD platforms such as YOUTUBE and SVOD platforms such as Lovefilm are now adding premium transactional VOD (TVOD) in order to handle current films. And as above, SVOD players are expanding their offerings beyond just library titles, beginning to buy newer and newer films in order to compete against premium PAY TV. This trend is continuing in the newer launching countries, e.g. Holland and Brazil where new PAY TV and localized SVOD and AVOD entrants have launched (e.g. YouTube regional sites). YouTube is also commissioning Made for Web content (MFW), although first in English language countries.

Festivals: Some European festivals have also recently started offering select titles on a TVOD basis. Rights Stuff recently worked with IDFA.tv to put around 100 films online—some on an AVOD basis and some on a TVOD basis—and in future more will follow. Certain other festivals (such as IFFR) have also begun to follow the US festival path of offering limited TVOD around or during the festival. This can open many doors for filmmakers, but also requires careful juggling and balancing when figuring out distribution patterns for conventional vs. online and new media….the balancing act is always key.